There’s one discussion that’s been going on for lifetimes & it’s about what’s best for generating & storing wealth.

Which is better? Investing, or saving?

I want to emphasise that there’s no right or wrong.

Do I have a personal preference?

Yes, but everyone is different.

Let’s go over the pros and cons of both, so you can make the decision for yourself on whether to save, invest, or both.

It’s all about identifying which factors apply to you, your situation, & your goals.

My personal opinion?

I do both, to an extent.

Sure, I invest a large proportion of my disposable income for the long term.

But, I still have an emergency fund which I can access in case a sudden expense arises, or if I want to buy something I like.

This way, I get the best of both methods.

Do I recommend it?

Sure, but only you know what is best for you.

Benefits of Saving

Let’s outline the key positive aspects of saving your money, or keeping your money in a bank.

Risk

I want to begin by outlining the risk, or the lack of risk with saving.

This is without a doubt the key reason why most choose to save over invest.

There is zero risk of losing your money with saving. You know exactly what you’re getting.

The money in your account will never decrease, unless interest rates become negative.

It’s safe & you’re able to check this as much as you like nowadays, with mobile banking.

A lot of people will turn their noses up at investing their money, because of the risks involved, which is fair.

Nobody knows where the prices of assets are going, especially in the short term.

You can look at historic data to prove that over time, investing has been superior.

But, there’s no way of telling where markets may go for now.

Of course, not every investment comes with the same level of risk.

Certain index funds are very safe & offer healthy annual returns.

Despite this, if you’re not willing to expose your capital to even small risks, it’s best to keep your money in a bank.

Accessibility

The accessibility of your capital, or liquidity, is also a huge factor.

With a bank account, or savings account, you’re able to access your money whenever, and wherever you want. This is something that you don’t get with investments.

You can sell your assets & withdraw the assets, but this could take days, depending on the type of asset you’ve sold.

If there’s something new…

A new game

A new pair of shoes etc.

…and it’s something that you want to buy, it’s easier to do so with savings.

This is why I have a small savings fund which enables me to buy things that I want, without selling my investments.

Zero risk. More accessibility.

Time

Let’s now talk about time.

One of the biggest assets an individual can have when investing is time.

Time to take advantage of market returns, and what Einstein called the eighth wonder of the world…

Compound interest.

But, depending on who you are, you might not be willing to invest this amount of time into your money.

If you think that the time you’d need to see returns is better off invested elsewhere, then investing may not be for you.

You may wish to choose to invest your money into… yourself. Starting a business, or buying educational books etc.

Returns

For a large period of my life, & yours too, interest rates have been 0%.

What this means is that banks have no obligation to give you any interest on your savings.

The interest rate is the base rate, or minimum rate set by the central financial entity.

As a result, for the past 15 years, we haven’t had any returns on our savings.

In 2022, base interest rates began to increase to combat surging inflation.

It was the first time in years, and depending on where you’re from, the base interest rates sit at around 2–5%.

You’re now getting a small return on your savings, which is something a lot of people have not seen for a long time.

You have security, accessibility, & now, a small return rewarding you for saving.

In the current economic climate, saving is a very smart option.

When interest rates were 0%, & investments were performing, it was a different story. But, the argument is very dependent on the present economic climate.

One thing we recommend is to keep in the loop regarding economic conditions.

Rates of inflation and interest change all the time. There are periods of time when saving is superior, and other times when investing is superior.

Make sure you stay in the loop.

Drawbacks of Saving

The first drawbacks to discuss, lie within the short term nature of said benefits.

Only a few of the benefits have long term effects. They’re beneficial because of the current economic climate.

Poor Long Term Rewards

The intervention that governments & central banks introduce to reward those who are saving.

Inflation had to slow.

The solution?

Increase the incentive for people to keep their money in the bank.

Interest rates have been non-existent for years, and only went above about 0.5% (at least here in the UK) in 2022.

Because of this, savers haven’t been generating a return on their disposable income.

Sure, take advantage of it whilst it’s here. But, there will come a time where interest rates start decreasing again.

Think of the economy of a ferris wheel.

When it’s going too fast, we need reform to slow it down… but not enough reform to stop it completely.

There will come a time where inflation is stable, and banks need to lower interest rates to increase spending.

This emphasises the importance of keeping up to date with current affairs. Especially key economic figures on inflation & interest rates.

If you have a long term outlook, interest rates will never compete with stock market returns.

If you’re willing to leverage time, holding assets like stocks & ETFs will be superior.

Inflation

On top of this… you have the one component of cash itself that is the biggest drawback to saving.

The invisible tax… Inflation.

Central banks can print money on demand, increasing the supply and reducing the value of your savings.

New cash gets printed all the time. In other words, any cash you hold goes down in value… all the time.

The rich get richer… because they own assets which go up in price.

The poor get poorer… because their savings lose value.

This is purchasing power, & the purchasing power of fiat currency is always decreasing.

When inflation is 10%, (which is extremely rare, but has occurred) it’s what you’re able to buy with the money that decreases by 10%… leaving you with an amount of money that is 10% less valuable.

Saving is not beneficial with a long term outlook.

Inflation will kill the value of your savings.

Some say that over a longer period, the bigger risk is not investing, because of inflation.

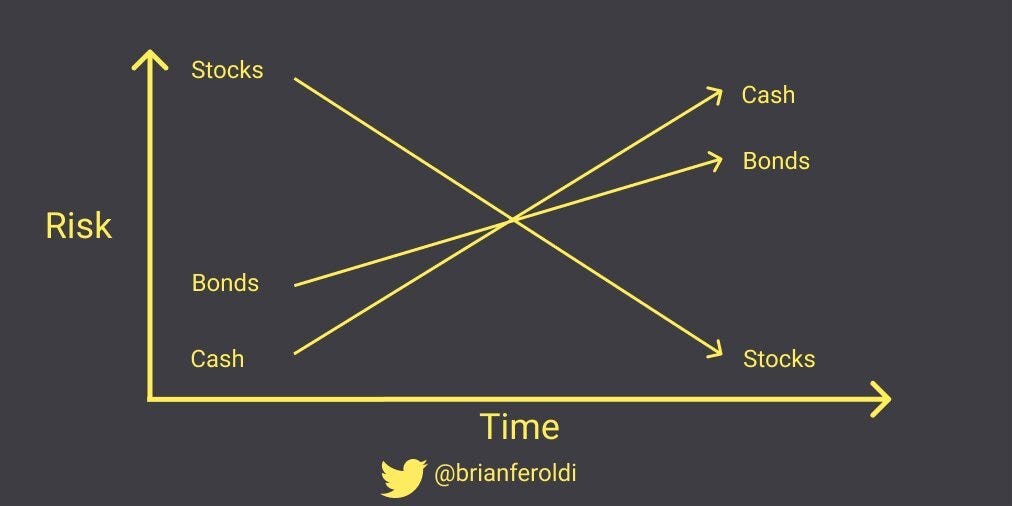

I love this visual from Brian Feroldi.

Because of economic factors, there are short term windows where saving is better. But, that’s it.

The only time saving beats investing is when inflation is high, & interest rates are going up.

There are only certain economic situations that favour those who save.

I must say, they don’t come around very often.

There’s a valid reason why the wealthy store their excess capital into assets, rather than cash.

It’s because they understand inflation, & the limits there are to holding cash.

Saving for a long period will not give you the returns you desire. It’s only beneficial to those who aren’t prioritising a return on their capital.

This is fine, and it depends on what you want out of your disposable income.

If you have other priorities, such as…

Security

Accessibility

Safety & No Risk

…saving is definitely superior to investing into assets.

Benefits of Investing

I may find myself repeating certain things here.

The benefits of investing are much like certain drawbacks of saving.

It’s important to look at them from a different perspective & talk about why these things occur.

Also, how individuals can benefit from investing their money.

Long Term Returns

The main selling point for investing is the power it has over longer time periods.

Putting your money into assets like:

Stocks

Index funds

Real estate

Is the only way that you’ll be able to beat inflation in the long term.

Inflation, as mentioned earlier, is the invisible tax. Those that save, are losing to inflation.

This may not be an issue if your outlook is short term, and for example, you’re saving for a car etc.

But in the long term, investing is the best option for generating & preserving wealth.

If inflation is at 5%, you need a 5% return on your money to be able to afford the same things as the year before.

The economics surrounding fiat currency, means savers lose in the long run.

The biggest issue many people have, is that only very few know about this, and very few are taking action against it.

The only ones that benefit from saving… are the banks.

What happens to your money when you give it to the bank?

It’s invested. It’s converted straight away. Without hesitation, out of fiat currency.

Why?

Because we have a monetary system designed to ensure the rich keep getting richer.

Why? Because they invest, & the poor keep getting poorer, because they save.

A bank is like any other shop, wanting you to buy their product or service.

The biggest issue is that so many don’t have the knowledge of an alternative.

Sure, we all need bank accounts & fiat currency to pay for bills & regular goods. But, if we’re talking disposable income… this is not what you should use a bank for.

The term “currency” comes from the term “current.”

Money is a medium of exchange, & the purpose of money is to exchange it for goods.

The purpose of money is not for wealth creation.

There’s a quote I have recently read, & it made me think a lot. I’d like you to think about this too…

“People don’t earn their way to success. They own it.”

It’s the knowledge, or lack of it, that stops so many from investing.

The only thing stopping a lot of people, is the lack of knowledge.

The idea of inflation isn’t new to a lot of people. But, its significance is underrated.

Especially when the inflation of prices compound over a long period of time.

Compound Interest

I want to dive into the idea of compound interest, which is another bonus of long term investing.

Compound interest, over a time, can give patient investors huge returns on investments.

Earning interest on your initial investment, plus any interest already earned.

By reinvesting your returns, you can build a portfolio that is always growing.

Imagine rolling a small snowball down a snowy hill. By the time it reaches the bottom, the snowball will be the size of a house because of all the snow it picked up.

This is how compound interest works…

Sure, you need a lot of conviction. But, the rewards of putting your money to work over a long period of time are life changing.

Long term investors have been enjoying compound interest for decades.

It’s all about beginning to invest as soon as possible.

Compound interest isn’t made through money. It’s made through time.

When you invest, you’re a beneficiary of compound interest.

When you save, you’re a victim of it.

Drawbacks of Investing

Higher Risk

Nobody knows where the prices of assets are going, especially when looking at a short term period of time.

Uncertainty is common. It can be very hard to paint a realistic picture of short term economic outcomes.

Sure, we can look at historic data to prove that over time, investing has been more lucrative than saving. But, there is no way of telling where markets may be going for now.

There’s always a small amount of uncertainty with the performance of investments.

One example was the morning my entire Twitter feed was full of news outlets reporting on Russia invading the Ukraine.

It was a terrible day for investments, regardless of where you were in the world. Sure, tensions were rising in the region…

But a full scale invasion?

You can’t prepare for events like these as a retail investor.

This puts an emphasis on the idea that you can’t invest with the hope of getting good returns in a short period of time.

Sure, it’s possible, but a short term mindset can be more damaging than beneficial.

We talk about the “time” needed to see the true benefits of investing.

If you don’t have time, or aren’t willing to invest it, you’re better off saving.

Once again, it comes down to your preferences.

If your outlook is short term…

The risk/reward of investing for a year, with the intention of selling regardless, isn’t worth the risk.

Take 2022 as an example of this. Even some of the safest index funds lost 15–20%.

Are long term investors worried?

No, but if you only intend on investing for a small period of time, it’s better off in the savings account.

Lack of Versatility

As well as this, money in investments lack the accessibility of savings due to liquidity.

When investing, you need an emergency fund in case an unexpected cost or expense arises.

The last thing you want to have to do is to sell any of your investments.

The whole idea is that you want to hold your investments for a long time.

You shouldn’t be investing money you need for bills or expenses etc.

But, with saving, you’re able to do whatever you want with your money, all the time. You don’t get this luxury with investing.

In other words, cash is more versatile than assets.

When it comes down to the topic of risk/reward, it’s this:

Short term: saving.

Long term: investing.

What is the method that you would rather choose?

Are you happy to take advantage of the historic price increases of assets, even if there are short term risks?

Are you happy with keeping your money in a savings account, even if you might be losing out to inflation in the long term?

Overall Assessment

There isn’t one method that’s better than the other. It’s all a matter of perspective & personal choice.

Me?

Sure, I am investing. I hate saving large amounts, because of inflation.

But I know that there’s millions of people out there that prefer saving because it’s safer. They can spend their money whenever they want & it’s easier.

Do I look at them funny for doing so? Of course not!

Everyone has different preferences & objectives.

If I had to recommend something, it would be to do both. Or, at least try investing if you haven’t done so.

If you don’t like the risk, or it makes you feel uncomfortable, that’s fine. Sell your assets & continue to save.

Knowledge is key, and it’s super important to do sufficient due diligence on the assets that you want to invest in.

It’s easy to make mistakes when investing. Make sure you’re in the best position to minimise these, or avoid them altogether.

Saving:

Risk — Long term risk. (inflation)

Reward — Short term reward. (interest rates)

Accessibility — Much superior accessibility.

Time — Worse over time.

Investing:

Risk — Short term risk.

Reward — Long term reward.

Accessibility — Longer to access & dependent on the investment.

Time — Better over time.

Thanks for reading! Be sure to subscribe (it’s free!) for more financial wisdom every week.