I’ve been investing for several years now, and in a way, my strategy has come full circle.

From spending hours researching investments, to not looking at it at all.

Like literally, I don’t look at it at all.

I still invest regularly. But, there’s no need for me to look at something that won’t change.

Regardless of how much I try to channel non-existent magic powers to try and make the number on my screen bigger.

Investing is becoming over complicated, and you don’t need to spend any time buying and selling.

All you need is a strategy that’s worked over generations, helping you minimising risk and maximise returns:

Dollar Cost Averaging.

What Is Dollar Cost Averaging?

Dollar Cost Averaging is a simple concept. It involves spreading your deposits over a large period of time, rather than going “all in” at once.

Let’s face it. Nobody has a clue where the markets are headed in the short term.

I still remember the day Russia invaded Ukraine. I’ve never seen anything like it.

The panic was incredible, and rightfully so.

Could you imagine how you’d feel if you invested all your money the days before, and then experienced a 15%+ drop within a day?

I wouldn’t wish it on my worst enemy. Well, actually maybe I would.

But this is why everyone should implement the simple DCA strategy. Rather than investing a lump sum, invest smaller amounts at regular intervals.

Typically, investors do this on a monthly basis.

Benefit of Dollar Cost Averaging.

The key benefit of DCAing is one thing: Minimising risk.

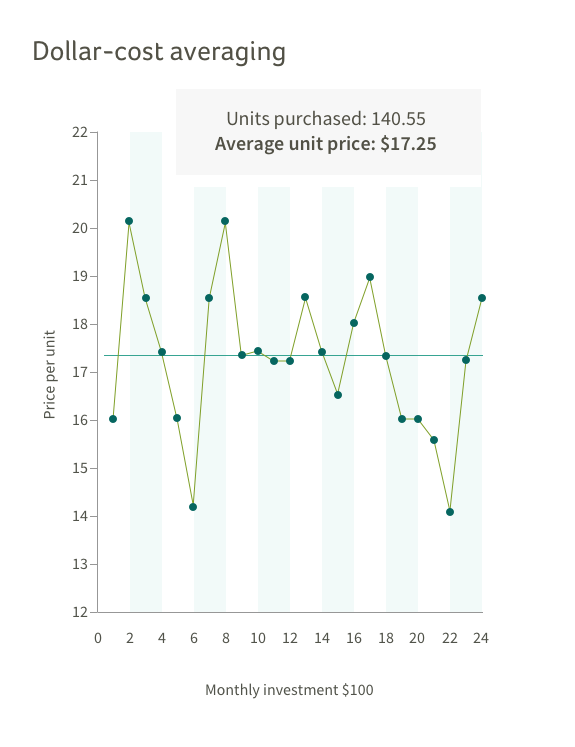

Dollar cost averaging in effect.

This investor is sitting at a healthy profit, with an average price of $17.25. And the current price of said investment is around $18.50.

Amount invested = $2,400 ($100 x 24 months)

Investment value = $2,600 (140.55 x $18.50)

The little dots represent monthly investments. You can see that this person has invested $100 a month, at a number of different prices, varying from $14 to $20.

As a result, investing in intervals has led to a healthy profit, rather than going “all in” anywhere above $18.50.

But it starts at $16?

If they went “all in” at the start, they’d have a better return…?

Of course, you’d be right, but… Hindsight is wonderful when investing.

There are hundreds of different scenarios that could’ve happened here.

What if this person invested 10% at $16, and then the other 90% at $20 expecting the price to continue rising to $25 or $30?

They’d still be at a loss, with no excess capital to continue investing at lower prices.

It’s as likely, but DCAing eliminates the “what if”.

It disregards all these risky scenarios by investing regularly at many price points.

When investing your hard earned money, why leave it to chance?

Implement the strategy of investing at regular intervals to minimise the risk of losing money.

How to Start Dollar Cost Averaging

If you’re not already using the DCA method…

The first thing to do is to decide on a regular (say, monthly) sum of money you wish to invest.

Rather than being in the mindset of “I want to invest $5k”, switch this to “I want to invest $100 a month.”

Instead of a lump sum, think long term, and think regular deposits.

It doesn’t need to be the same each month. If you’re new to investing, start small, and increase your deposits as you become more comfortable.

Automate Your Investments

Many platforms enable you to set up automatic direct debits so you don’t have to make the deposits yourself.

Just like any other monthly expense. Perfect.

Money goes out of my bank account and into my Stocks & Shares ISA each month without me having to lift a finger.

I like the efficiency of this.

You’re still able to get healthy returns, whilst not investing any time.

You can then use this time in other areas.

Starting a business

Learning something new

Playing COD

Whatever takes your fancy.

Final Thoughts

If you’re not using the DCA strategy, you’re exposing your investments to unnecessary risk.

Who knows where prices of assets are going for now.

What’s important is having a constant revenue stream for eating up potential declines.

Rather than going all in & having your pants pulled down if prices tank in the short term.

I invest for the long run. I’m of the mindset where if I see a decline, I see this as a great opportunity to buy more & lower my average buying price.

How am I able to continuously buy dips?

Because I dollar cost average.

Thanks for reading! Be sure to subscribe (it’s free!) for more financial wisdom every week.