- The Financial Revolution

- Posts

- How to Create A Budget That Works

How to Create A Budget That Works

Implementing a winning budget formula to help you achieve your financial goals.

Jack Spicer

January 03, 2025

Budgeting is a crucial aspect of building wealth and levelling up financially in 2024.

Despite this, a lot could go wrong if you’re unsure how to create a simple budget to help you track:

Income

Expenses

Disposable Income

And more.

So, I’m going to walk you through, step-by-step, the budget that helped me turn my life around financially.

But first…

What is a budget?

A budget is a method used in finance to track a person’s overall finances on a monthly basis.

Income

Expenses

Savings

And more.

They’re used to help people gain a better understanding of where you’re spending your money, and how to increase your disposable income each month.

They’re not glamorous, but they are useful, and can be significant in ensuring financial discipline whilst building wealth and walking the path to financial freedom.

You can create a budget anywhere you like. It’s up to you:

Excel sheet.

Pen and paper.

Online budget template.

So, if you’re ready to start creating your budget, let’s begin with the first step.

Objective

The first thing to complete when creating a budget is to come up with a realistic, yet ambitious objective.

Why should you come up with your objective before you do anything else?

Because you don’t want your current financial situation to have an impact on your overall goal.

Say you want to increase your disposable income to 20%, but you’re currently only on 5%, setting your objective first will help you take more drastic action to achieving your goal.

But, if you first find out you’re only saving 5%, you might adjust your objective to only 10%, ultimately falling short of what you really want.

So, think of an objective before you do anything else. Most objectives will be related to disposable income: your income minus expenses.

I want to save 10% of my income to invest into ETFs.

I want to save 5% of my income to pay off credit card debt.

I want to have 10% disposable income to build an emergency fund of 3 months, and then save for a deposit on a house.

Me? I like to have my objective split into three sections.

A popular budget format is known as the 50/30/20 budget, and this is a budget I’ve followed for years to keep my expenditure in check.

50% — Needs.

30% — Wants.

20% — Savings.

So, in effect, my objective is to ensure I have 20% disposable income at the end of each month, so I can invest for my future.

Got your objective? Perfect. Let’s move on.

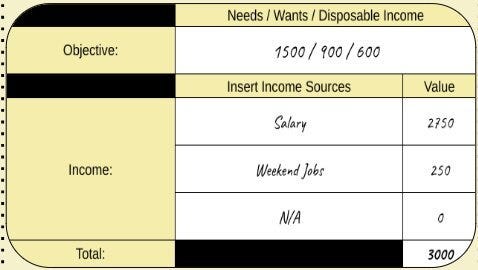

Income

Your next step to complete is your income.

Assuming most of you will only have 1 income source (your salary) this won’t take very long.

If your income fluctuates, it’s best to take an average over a longer time frame. The longer the time frame, the more accurate it’ll be.

Up to this point, your budget should look a little like this:

My objective was to save 20% of my income.

Expenses

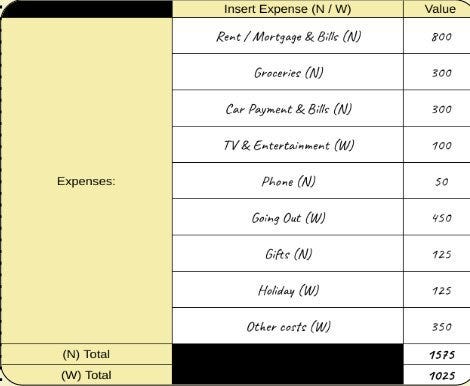

Labelling your expenses is the longest and most important part of your budget.

I must emphasise that it doesn’t need to be detailed, but it does need to be accurate.

Go through your recent bank statements and fill out your expenses for the month.

It’s always a good idea to label them as needs (N), wants (W) and savings (S) if you’re using the 50/30/20 format I spoke about earlier.

Once you’re done, you should have something a bit like this:

Remember to split your expenses into needs, wants and savings.

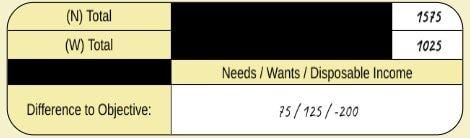

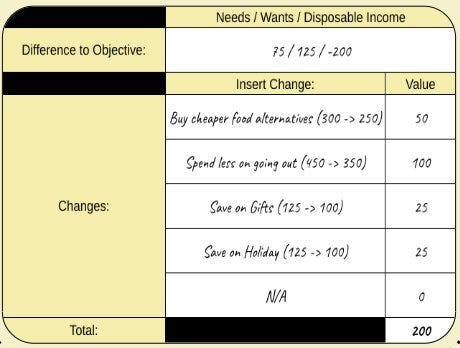

Difference to Objective

Now you’ve calculated your expenses, you can go back to your objective to see how close (or, how far) you are from reaching your ideal level of expenditure.

As you can see, for this example:

Overspending by $75 on needs.

Overspending by $125 on wants.

Underspending by $200 on savings or investments.

Some spending habits will have to change.

Making Changes

Once you know the difference to your objective, it’s now all about implementing changes necessary to reach your objective.

How much you change is all down to how close you are to your expenses.

Remember, your objective comes above everything. Nothing should get in the way of you reaching this target.

If you’re struggling to find ways to reduce expenses, remember the alternative: increasing your income.

Side hustles.

Starting a business.

Job hopping.

These are all possibilities, but will require you to invest your time to see returns.

But, the easiest way to increase your disposable income, is to reduce your expenses.

You’re making financial sacrifices, rather than investing time which you might not be willing to do.

Changes made. Objective reached ✅

Implementing Your Budget

Creating a budget is important, but do you know what’s more important?

Implementing your budget with effect.

Here are some key budgeting tips to help you on your journey:

Start Straight Away.

Chances are, the objective of your budget is to save more money.

Because of this, there’s no need to wait for the perfect moment to start implementing.

Just do it right away.

It doesn’t have to be perfect, but if you start as soon as you can, you’ll quickly begin to see changes to your expenditure, and disposable income will begin to pile up.

Review and Change Regularly.

Our lives are always changing, and with that, comes changes to our expenditure. It’s worth reviewing your budget on a monthly or quarterly basis to:

See what’s working.

See what’s not working.

Simple as that.

Remember… it’s your life.

If you don’t want to cut down on something, that’s fine, but if you’re set on reaching an objective, you should always prioritise this.

Prioritise Consistency Over Perfection

It doesn’t matter how pretty your budget is.

What matters is that you’re implementing it, and seeing results.

It’s never going to be perfect, and will probably be a working progress for a while.

but, that doesn’t matter.

As long as you’re working towards that objective, you’re making progress, and that’s all that matters.

Thanks for reading! Be sure to subscribe (it’s free!) for more financial wisdom every week.

Reply